Fusion Micro Finance IPO: All You Need to Know

The second IPO of the week is here! Financial services firm Fusion Micro Finance has launched its three-day initial public offering (IPO) today— Nov 2. In this article, we shall analyse the company and its IPO.

Company Profile - Fusion Micro Finance Ltd

Established in 1994, Fusion Micro Finance Ltd (FMFL) provides financial services to women entrepreneurs belonging to the economically and socially deprived section of society. Its network and services have improved accessibility to formal credit (loans) at affordable rates, thereby positively impacting the lives of people in rural India. Apart from financial support, FMFL also offers financial literacy sessions.

FMFL’s business runs on a joint liability group-lending model— a small number of women form a group (comprising 5-7 members) and guarantee each other's loans. The company has primarily focused on strategic geographic diversification with a rural focus, embracing technology for growth, nurturing & developing personnel, and careful risk management.

Factsheet:

- The microfinance institution (MFI) currently has nearly 29 lakh active borrowers.

- Its total assets under management (AUM) grew from ₹4,673.84 crore in FY21 to 6,785.97 crore in FY22. As of June 30, 2022 (Q1 FY23), the company’s AUM stands at ₹7,389.02 crore.

- Bihar, Uttar Pradesh, Odisha, Madhya Pradesh, and Tamil Nadu cumulatively account for 66.12% of its AUM.

- As of Q1 FY23, FMFL has 966 branches and 9,262 permanent employees spread across 377 districts in 19 states and Union Territories in India.

- The company had the fourth fastest gross loan portfolio CAGR of 53.89% between FY17 and FY21 among the 10 largest NBFC-MFIs in India.

About the IPO

Fusion Micro Finance Ltd’s public issue opens on Nov 2 and closes on Nov 4. The company has fixed ₹350-368 per share as the price band for the IPO.

The fresh issue of shares (of the face value of ₹10 each) aggregates to ₹600 crore. The IPO also includes an offer for sale (OFS) of 1.37 crore shares by promoters and early investors. Individual investors can bid for a minimum of 40 equity shares (1 lot) and in multiples of 40 shares thereafter. You will need a minimum of ₹14,720 (at the cut-off price) to apply for this IPO. The maximum number of shares that can be applied by a retail investor is 520 equity shares (13 lots).

FMFL will utilise the net proceeds from the IPO to augment its capital base.

The total promoter holding in the company will decline from 85.57% to 58.1% post the IPO.

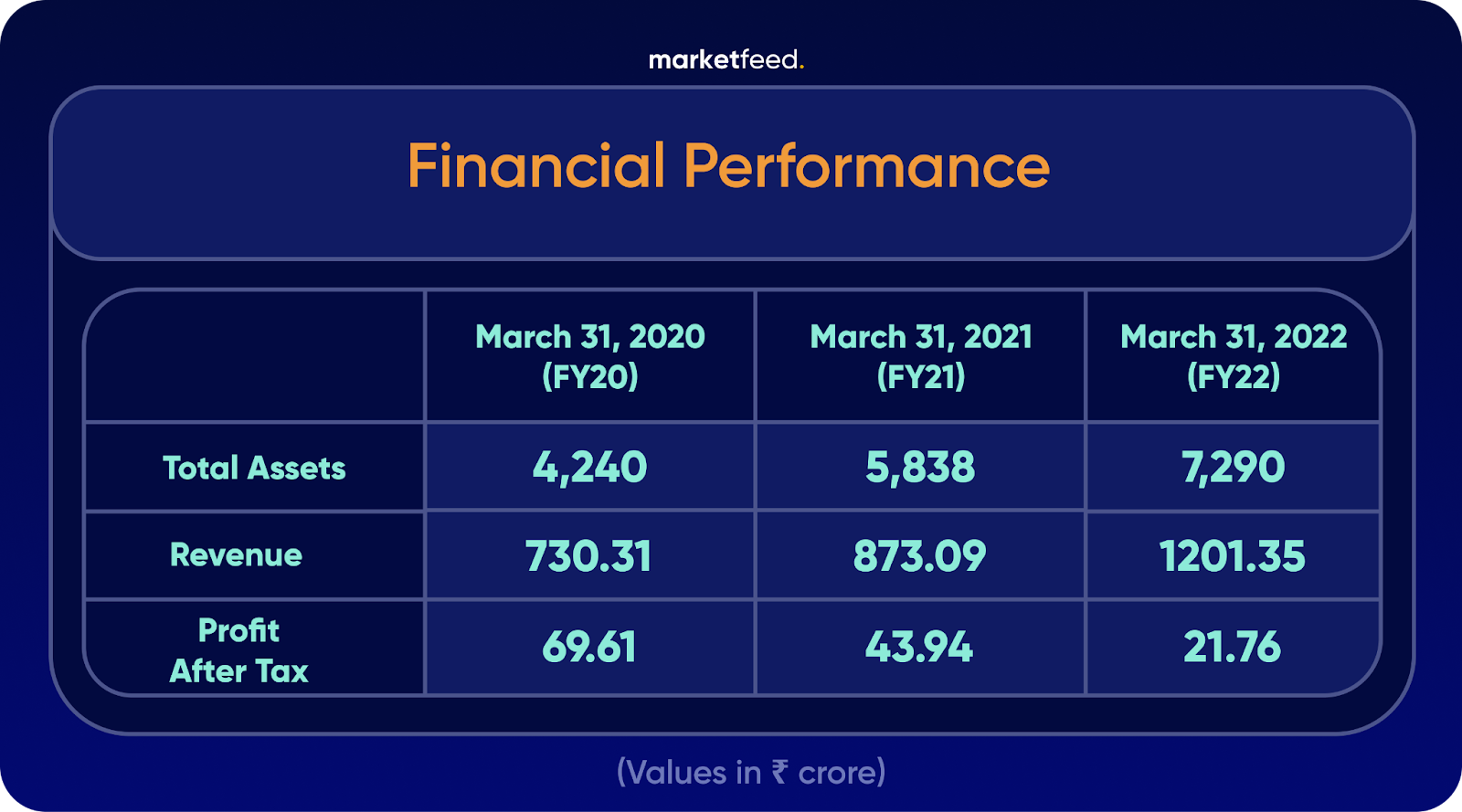

Financial Performance

Fusion Micro Finance’s profitability was impacted by higher provisioning due to the Covid-19 pandemic and branch expansions. However, the company’s net profit improved from ₹4.41 crore in Q1 FY22 to ₹75 crore in Q1 FY23, owing to higher interest income and lower provisions. Its revenue has increased at a compound annual growth rate (CAGR) of 26.44% over the past three financial years (FY20-22).

Between March 31, 2016, and June 30, 2022, the number of active borrowers grew at a healthy CAGR of 33.63%, while the number of branches grew at a CAGR of 31.92%.

FMFL’s capital adequacy ratio (CAR) has remained strong. It stood at 21.13% as of Q1 FY23. [Higher CAR indicates that the bank is in a better position to deal with unexpected losses due to availability of adequate capital.]

Risk Factors

- An increase in the level of non-performing assets (bad loans) or provisions may adversely affect FMFL’s business and financial performance.

- A significant portion of the company’s customers is located in rural markets. It may face difficulties in conducting operations and implementing technical measures in such markets due to limited infrastructure.

- The inability to manage its growth effectively or sustain historical growth rates may severely impact FMFL’s overall business.

- Any failure or security breach in the firm’s information technology systems could harm its reputation and credibility.

- Any downgrade of Fusion Micro Finance’s credit ratings may constrain its access to capital and debt markets. It may affect its cost of borrowing and financial condition.

IPO Details in a Nutshell

The book-running lead managers to the public issue are ICICI Securities, CLSA India, IIFL Securities, and JM Financial. FMFL filed the Red Herring Prospectus (RHP) for its IPO on Oct 25. You can read it here. Out of the total offer, 50% is reserved for Qualified Institutional Buyers (QIBs), 15% for Non-Institutional Investors (NIIs), and 35% for retail investors.

Conclusion

Going forward, Fusion Micro Finance plans to grow its business by attracting new customers in existing markets that remain relatively untapped. It has a social vision to provide economic opportunities to underprivileged women and transform their quality of life. FMFL will also enter new regions with lower penetration of microfinance firms. They will continue to automate and digitise various aspects of the business. In terms of financial performance, FMFL is on a recovery path as indicated by Q1 FY23 results.

CRISIL Research expects the MFI industry to grow at 18-20% CAGR between FY22 and FY25. During the same period, NBFC-MFIs are predicted to grow at a much faster rate of 20-22%.

FMFL faces stiff competition from listed peers such as Credit Access Grameen Ltd, Spandana Sphoorty Financial Ltd, Bandhan Bank, Ujjivan Small Finance Bank (SFB), Equitas SFB, and Suryoday SFB.

The company has received some interest in the grey market. FMFL’s IPO shares are trading at a premium of ₹35 in the unofficial market. Before applying to this IPO, we will wait to see if the portion reserved for institutional investors gets oversubscribed. As always, do consider the risks associated with the company and come to your own conclusion.

What are your opinions on this IPO? Will you be applying for it? Let us know in the comments section of the marketfeed app.

Unlock extra income via

Unlock extra income via Automated TradingLearn how marketfeed can help

grow your wealth

Post your comment

No comments to display