Options Greeks: What is Theta?

Before you go through this article, we request you to go through the basic terms of Options. You can find it here. If you are learning about options, you have to be thorough with the knowledge of Option Greeks. It helps the trader to know how and why the price of the options changes. So let us learn about what theta is, known as an option seller's friend and an option buyer's worst enemy.

We will start this series by explaining one of the most important Option Greeks, which is the Theta or time decaying factor. Both Call and Put options lose value as the expiry date nears. The rate at which they lose value is called Theta. A Theta value of -2 indicates that the option premium will fall by Rs 2 each day which is passed. But why do the options lose value? Let's find it out here.

Explaining Theta

How important is time? Does time have a cost? If yes, how will you associate a price with time? Before you read forward, take a minute and form your own opinion on these three questions.

Let's look at an example. Imagine you want to become an established cricketer in the Indian team. How would that happen? You have to put in years of practice and learn many skills. You have to devote your time day in and day out to become a better cricketer. Still, there is no guarantee that if you decide to give 20 hours each day, you will be selected for the national team.

But, you will surely have a better chance of becoming a cricketer if you spend your time upskilling yourself rather than doing absolutely nothing in the field. Thus, the likelihood of you becoming a cricketer directly correlates with the time you put in. Similarly, you will be more confident about an exam if you have more days to study for it. Why? This is because you would feel that you have an ample amount of time to prepare for it. The longer the time for preparation, the more confident you will be.

This same logic is followed in the stock market as well. Suppose Nifty 50 is around 13,500. You have two options contracts among which you can buy anyone. Firstly, Nifty 14,000 Call Option which expires in 2 days. Secondly, Nifty 14,000 Call Option which expires in 20 days. Obviously, you will feel safe and confident in buying the second Call Option. Why? This is because more the time, the better the likelihood for the index to move up. In short, more time to expiry leads you to have a better chance of ending your position in profits.

Risk of an Option Seller

All the conversations we had above were from the perspective of an option buyer. Now, let's switch our hats to that of Option sellers/writers. As an Options seller, you don't want the Nifty to cross 14,000 in the above example. If Nifty crosses above 14,000 then you have to pay money to the option buyer. If Nifty remains below 14,000 points, you will get to retain the option premium you received from the buyer.

Out of the two Call Options, in which one do you feel the risk for you as an option seller is higher? Yes, it is the second one which is riskier. Nifty crossing 14,000 points in 2 days has a lower probability than it crossing that mark in 20 days. What do you want to compensate for this risk? Money! This concept in the world of finance is known as Time Risk. Options premium is always the summation of the intrinsic value of your option and the time value involved.

Option Premium = Time value + Intrinsic Value

Hence, one can easily draw a conclusion from this. If you are buying a call option with a farther expiry date, then you are obliged to pay a higher option premium for it. This higher option premium is paid to compensate for the Options Writers' time risk.

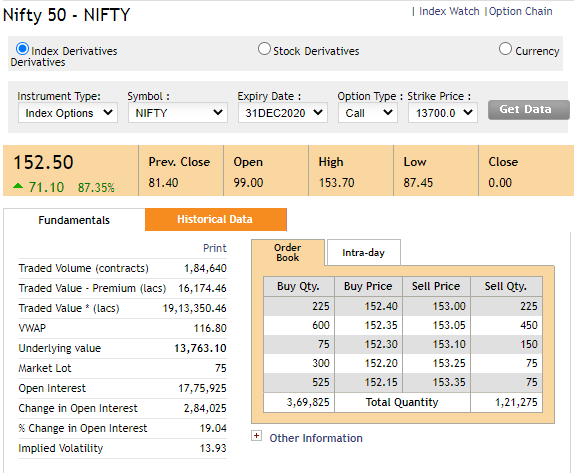

The chart below shows the Nifty option chart with a strike price of 13,700. The expiry date of this Call Option is 31st December 2020. The Option Premium which the buyer has to pay to the writer is Rs 152.50.

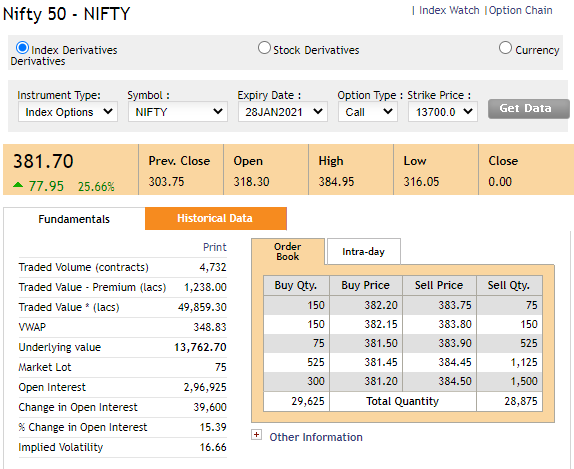

The second chart shows the Nifty Call Option with the same strike price but with a farther expiry date. The contract has to be closed on 28th January 2021. The Option Premium which the buyer has to pay to the writer is Rs 381.79. Between the two Call Options with the same price, an option buyer has to pay a higher option premium to the option seller/writer for the contract whose expiry date is farther.

Conclusion

As the option reaches closer to its expiry date, the time risk of the option seller/writer decreases. Due to this, the option premium loses some of its time value. Thus, decreasing the option premium which has to be paid to the option seller/writer.

Theta is considered very difficult to understand. But in reality, it is very easy. Just remember that time has an opportunity cost and that cost is reflected in Theta. Wait for the next chapter of this series to get a better idea of what Options Greeks are. Till then, happy trading!

Unlock extra income via

Unlock extra income via Automated TradingLearn how marketfeed can help

grow your wealth

Post your comment

No comments to display