What is Cash Flow Statement?

A Cash Flow Statement is a vital document that provides a clear picture of a company's financial health. Whether you're a new or seasoned investor, it's important to understand the basics of a cash flow statement. In this article, we will understand what a cash flow statement is, its structure, and how to analyse it.

What is a Cash Flow Statement?

A cash flow statement provides information about a company’s cash receipts and cash payments during an accounting period. In simple terms, the statement shows where a company spends its cash and how much it receives. It contains details regarding net cash inflows and outflows of a company and the cash balance. They can be categorised into: cash flow from operating activities, cash flow from investing activities, and cash flow from financing activities.

Cash Inflow vs Cash Outflow

Cash inflow refers to the cash that a company receives during an accounting period, while cash outflow is the cash that a company spends during an accounting period. For example, a company bought 10 packets of milk for ₹200 and paid the seller ₹200 in cash. The company then sold 10 packets of milk to another person and received cash of ₹250. Here, the cash inflow and outflow of the company are ₹250 and ₹200, respectively.

Cash inflow is represented by a positive sign and cash outflow by a negative sign.

Why Should You Analyse a Cash Flow Statement?

A cash flow statement provides detailed information about the cash transactions of a company during a year. Only cash-based transactions are included in the cash flow statement. So the revenue earned by selling products and services on credit will not be included.

In the statement of profit & loss, revenue from operations includes both cash sales and credit sales. Credit sales are those in which the products were sold on credit, which means that a company will only receive cash after a certain period. On the other hand, cash sales are those in which the products are sold after the immediate receipt of cash. Revenue in the income statement shows the value of revenue earned even if the actual cash is yet to be received. Meanwhile, a cash flow statement only shows the amount of actual cash received for sales and does not include the value of credit sales.

Therefore, a cash flow statement helps investors to understand how a company’s operations are making money and how it spends. It also shows how efficiently a firm is managing and generating its cash and how it pays off debt and other obligations. A consistent positive cash flow indicates a healthy and sustainable business model. It reflects a company's capability to cover its operating expenses and invest in growth opportunities.

Classification of Cash Flows

All cash transactions are summarised in a cash flow statement by grouping each transaction into three categories:

- Operating Activities: This includes a company’s day-to-day activities that create revenue, such as selling products and services. There are cash outflows and inflows from operating activities. Cash inflows contain cash received from sales and debtors of the company, along with other cash income. Cash outflows contain cash spent or paid to generate sales. It includes transactions such as cash purchases, salary payments, marketing expenses, etc.

- Investing Activities: This includes purchasing and selling long-term assets and other investments. Cash received and paid for the purchase and sale of buildings, land, machinery, equity shares, and bonds of other companies, etc. The purpose of this activity is to gain benefits in the future.

- Financing Activities: This includes obtaining or repaying capital such as equity and debt. Cash inflows in this activity include the receipt of cash from issuing stock, bonds, etc. Cash outflows include cash payments to repurchase stock, repay bonds, pay interest & dividends, etc.

What is the Structure of a Statement of Cash Flows?

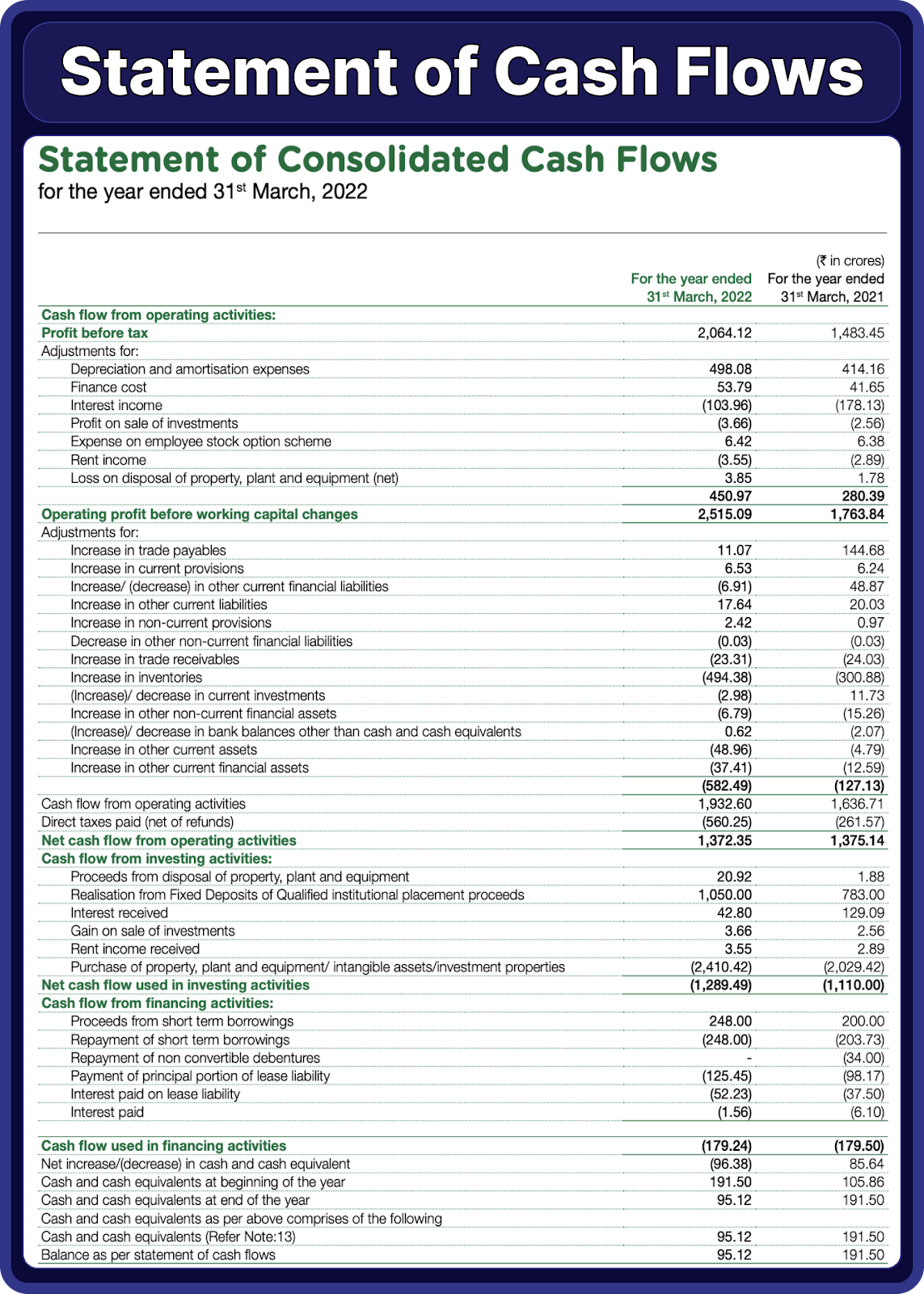

Let us understand different cashflows in detail by analyzing the consolidated cash flow statement of Avenue Supermarts (DMart):

Let us analyse each item in detail:

Cash Flow From Operating Activities

The net cash flow from operating activities is preferably positive in a cash flow statement as a company's core purpose is to bring in cash flow. All the adjustments regarding the operational cash flow of the company are shown in this section.

DMart’s cash flow from operating activities is positive, which is a good sign.

Cash Flow From Investing Activities

The net cash flow from investing activities can be negative and still favourable. When a company pushes cash outwards to invest in different assets, it will help them to grow further and generate even more cash flows.

DMart’s cash flow used in investing activities is negative, meaning that it is investing in different assets. The details under investing activities say that DMart spent ₹2,410 crore to purchase new properties, plants, equipment, etc.

Cash Flow From Financing Activities

The net cash flow from financing activities is favourable to be negative because it means that the company is spending money on its investing activities and the capital that it raised by borrowing money is being paid off.

DMart’s cash flow used in financing activities is also negative because it paid off a few liabilities.

Net Increase/Decrease in Cash and Cash Equivalents

It represents the sum of all three different cash flow activities in the company. This shows the total net cash that the company paid out or received during the financial year.

Cash and Cash Equivalents at the End of the Year

Net increase/decrease in cash and cash equivalents is subtracted from cash and cash equivalents at the beginning of the year to find the cash and cash equivalents at the end of the year. This will be the actual cash the company has in its bank account.

The final amount of cash that DMart has in its bank account after all the transactions in the previous year is ₹95.12 crore.

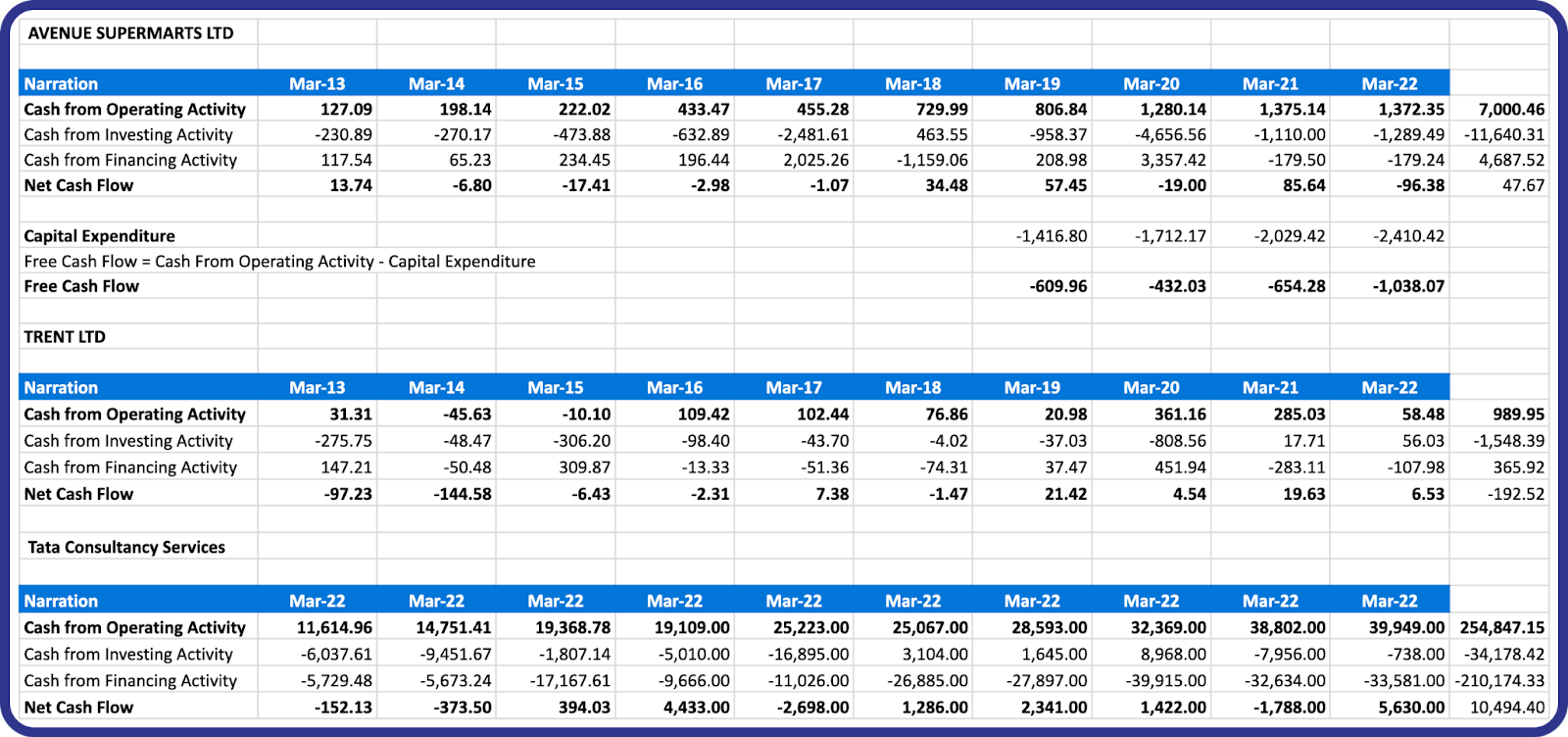

Using Cash Flow Statement as a Litmus Test

The data in the cash flow statement can be used to perform a “quality test” on the company. We can understand if the company is generating enough cash flow to sustain its operations. This test can be done by comparing the company with its peers, along with historical data. We can analyze if the net cash flow of the company has been increasing or decreasing over the years and if the cash flow from operating activities keeps on increasing and is positive. Spending cash on investing activities is very important because it increases the company’s ability to generate cash flow in the future.

By analyzing the previous 10-year data of the three different companies above, we can see that the operating cash flow of DMart has increased over the years, while the operating cash flow of Trent Ltd is not very good.

You can make decisions on whether to study a company by analyzing its cash flow data. You can skip analyzing the company if its cash flow is not good or justifiable.

What is Free Cash Flow (FCF)?

Apart from net cash flow and details of cash flows from different activities, another important metric that the cash flow statement provides is free cash flow. A free cash flow is the excess operating cash a company generates after accounting for capital expenditures such as buying land, building, and equipment. It is the cash available to a company to repay creditors or pay dividends and interest to investors. Veteran value investor Warren Buffet called it owner’s income and popularised it for stock analysis.

Free cash flow can be calculated using the following formula:

DMart’s free cash flow = ₹1,372.35 - ₹2,410,42 = - ₹1,038.07 crore.

Having a negative free cash flow is unfavourable for a company. It means that the firm is not able to generate enough cash from operating activities to meet its capital expenditures.

In this article, we learned what a cash flow statement is and how to analyse it. We also learned how to perform a litmus test to know if it is even worth considering. Make sure to download the cash flow statement of a company and try to understand it.

Unlock extra income via

Unlock extra income via Automated TradingLearn how marketfeed can help

grow your wealth

Post your comment

No comments to display