Trident To The Moon?

As investors, we always desire multifold returns on our stock picks. We are going through a massive bull run, and many quality stocks have given impressive returns to their shareholders. In this article, we shall analyse Trident Group, a company that will benefit from India being a global manufacturing and export hub. The stock has given a ~440% return to its investors within just a year! The market capitalization of the stock has crossed Rs 20,000 crore and will come under the large-cap segment.

Trident - A Brief Profile

Trident Limited commenced operations in 1990 and is headquartered at Ludhiana, Punjab. The company has three main business verticals:

- Home Textiles: Textiles that are used in homes, such as curtains, bed & bath linens, and pillow covers falls under this segment. Trident is a vertically integrated home textiles company. It has direct ownership in every step of manufacturing— from raw materials to finished products. This cuts down expenses, and the company is able to market its products at competitive prices. Terry towel, bath, and bed linen are the main products of the company. The vertical contributes 55% to the total revenue.

- Cotton yarn: The company manufactures cotton yarn for the home textiles segment as well as for the retail space. Nearly 27% of the total revenue comes from this segment.

- Paper & Chemical: Apart from the conventional way of paper manufacturing (from cellulose), Trident uses wheat straw (residue of wheat harvest) as the raw material. It includes the production of copiers, writing, and printing papers. Trident has also entered into the chemicals industry through the manufacturing of sulphuric acid.

Financial Performance

For the financial year 2021 (FY21), Trident reported a 4.2% year-on-year (YOY) decline in revenue to Rs 4,546 crore. The 5-year Compounded Annual Growth Rate (CAGR) of the revenue stands at just -1.27%. The CAGR tells us that sales of the company are not growing across the years.

The company’s Profit After Tax (PAT) also declined 10.4% YoY to Rs 304 crore. Similar to the revenue, profits have also not grown over the years.

Trident is an export-oriented company. Out of the total sales, 68% was attributed to customers outside India. The company caters to entities in the United States, Europe, and the Middle East.

Return on Equity (ROE) and Return on Capital Employed (ROCE) are profitability ratios. It helps to analyse the ability of a company to generate profit with respect to shareholder’s equity.

From the graph shown above, it is clear that there is no improvement in the profitability of the company. An ROE of 9% means that for every Rs 100 investment made by investors, the company can generate Rs 9 as net profit. In ROCE, we consider the overall capital (equity + debt).

The company has announced Vision 2025, through which it aims to achieve total revenue of Rs 25,000 crore with a 12% profit margin. In the current financial scenario, accomplishing the revenue target will be a mammoth challenge for the company.

Peer Competition

Since Trident has 3 business verticals, the manufacturer faces competition from different companies. Vardhman Textiles and KPR Mills are the competitors in the cotton yarn industry.

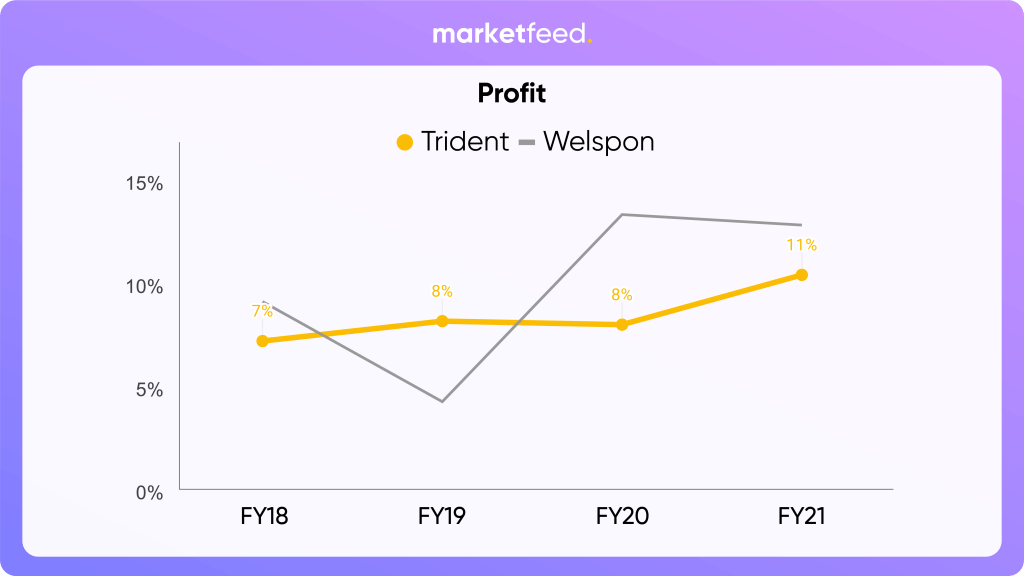

Let us look over the profit margins of the home textiles department with a strong competitor— Welspun India Ltd.

From the graph shown above, we see that both companies have a similar range of profit margins. Trident with a Profit Margin of 11%, which means that for a revenue of Rs 100 (after all the expenses), the company can keep Rs 11 as net profit.

Reasons Behind the Rally

There can be two reasons for a stock to move up— Technical and Fundamental.

Under technical analysis, it depends upon the supply-demand of the stock in the market as well as due to the breakouts or breakdowns of a price acting as resistance/support.

In the weekly chart, we can see how Rs 11 (a resistance formed over the past few years) broke out with a significantly large volume. This sudden increase in demand created in the markets makes supply short, and thus, the price went up.

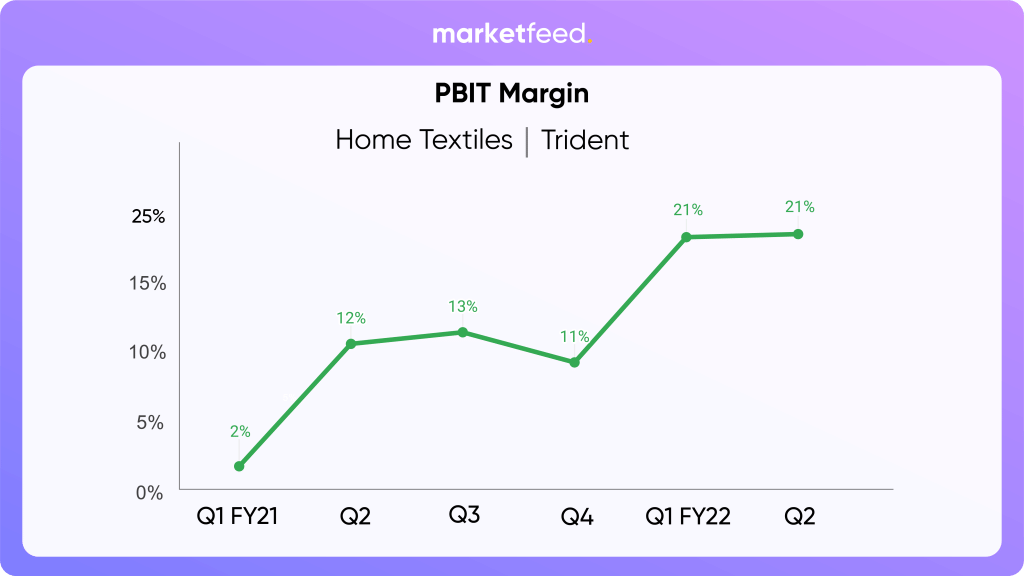

Now, what created this demand? The company’s third-quarter results were to be out on January 18th, and the sudden pulse in volume was observed in the second week of January. The result was not extraordinary; the company reported a decent 11% growth in the revenue from operations. Interestingly, profit margins of the home textile segment are picking up from the impact created by the Covid-19 pandemic. It may even be better than pre-pandemic levels.

Conclusion

The home textile sector is driven by the new hygiene-conscious lifestyle, increase in stay-at-home culture, and the arrival of the festive season. Across the globe, companies adopting “China Plus One” sourcing strategies have also developed new opportunities for Indian exporters like Trident. This can be observed by the increase in the market share of Indian companies in the global textile industry.

Moreover, rating agencies such as ICRA and CRISIL have rated a jump in sales of ~25% for Indian exporters in FY22, along with a healthy profit margin better than the pre-pandemic period.

Rally in Trident Ltd can be related to the upcoming demand for their products, along with a technical breakout in the stock that has been consolidating in a price range for a long period.

What are your views on Trident’s rally? Have you invested in the company? Let us know in the comment section of the marketfeed app.